After last year’s “third-time lucky” Budget, many predicted doom and gloom this year. There was talk of the need for an additional R20 billion of tax hikes – whether in the form of the much-maligned VAT increase proposal rearing its ugly head, or direct personal income tax hikes.

That didn’t happen. In presenting his 2026 Budget, Finance Minister Enoch Godongwana has attempted to strike a careful balance of avoiding major tax hikes while still raising revenue and stabilising the country’s finances. While it is far from being perfect, it does contain some welcome reasons for South African taxpayers to smile.

Here is a summary of how this Budget affects the group that ultimately contributes by far the largest share of South Africa’s tax revenues (whether through income tax, VAT, or other taxes and levies)—individual taxpayers.

No major tax rate increases

One of the most significant aspects of Budget 2026 is what it did not do. There was no increase in personal income tax rates, and no change to the VAT rate (which remains at 15%). In an environment where disposable incomes are already strained, this provides welcome stability for salaried workers and consumers.

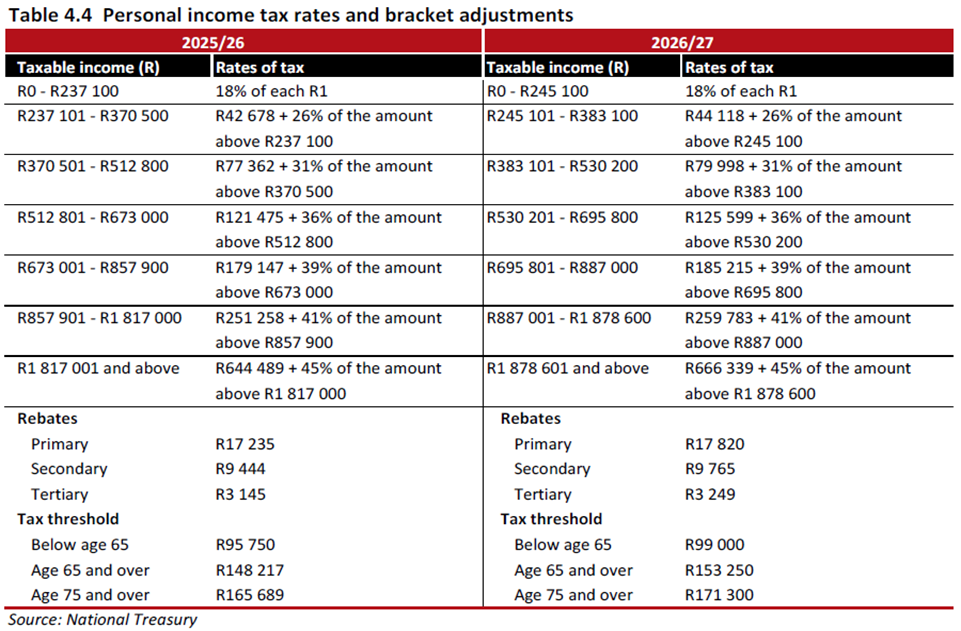

However, while rates were left unchanged, the extent of inflationary adjustments to tax brackets determines whether taxpayers experience ‘bracket creep’ (paying more tax simply due to inflation-related salary increases). For the last three years, the tax tables have been frozen.

Relief through adjusted thresholds

As already stated, the tax tables have been frozen since the 2023/24 tax year. The resultant ‘bracket creep’ has meant that salary increases have pushed many taxpayers into higher tax brackets, the result being that their take-home pay has actually decreased in real terms.

This year’s Budget has broken that trend, with the 2026/27 tax tables having had adjustments to the tax brackets and rebates. This helps prevent taxpayers from drifting into higher tax brackets due solely to inflation-linked salary increases.

The primary rebate and tax thresholds have also been adjusted to provide limited relief to lower- and middle-income earners. For retirees and individuals over 65, increased rebates offer modest protection against rising living costs.

Retirement and savings incentives

Government continues to promote long-term savings by maintaining favourable tax treatment for retirement contributions.

Up until the 2025/26 tax year, individuals have been able to deduct retirement fund contributions up to 27.5% of taxable income, subject to an annual cap of R350,000. This annual cap has been raised to R430,000 – the first increase in 10 years.

The retirement fund de minimis threshold for annuitisation has also increased from R247,500 to R360,000. This means that if your retirement fund value is less than R360,000 upon retirement, the full amount (rather than the maximum one-third) may be taken as a lump sum.

Tax-free savings accounts (TFSAs) remain attractive, allowing individuals to earn investment growth free of income tax, dividends tax, and capital gains tax within annual and lifetime contribution limits.

While the lifetime limit remains unchanged at R500,000, the annual contribution limit has been increased from R36,000 to R46,000.

Capital Gains Tax (CGT) relief

A number of changes to CGT thresholds have been introduced in this year’s Budget – many of which have not been adjusted since 2012.

Small business owners have historically been granted CGT relief when disposing of their business after reaching the age of 55, with the first R1.8 million of capital gain being exempt from CGT. This exempt amount has been increased to R2.7 million with effect from 1 March 2026.

The asset threshold below which a small business qualifies for such relief has also been increased from R10 million to R15 million.

For those who are disposing of their primary residence, the exempt amount increases from R2 million to R3 million. Such additional relief is welcome, given how house prices have increased over the past 14 years.

Finally, the exclusion threshold for capital gains at the time of one’s death has increased from R300,000 to R440,000, whilst the normal annual inclusion increases from R40,000 to R50,000.

Rewarding generosity

The annual exemption from donations tax for donations made by individuals has been fixed at R100,000 since 2007. This annual exemption increases to R150,000 as from 1 March 2026.

‘Sin taxes’ and fuel levies

Unfortunately, this Budget also contains the proverbial ‘fly in the ointment’ – excise duties on alcohol and tobacco have been increased again, broadly in line with inflation. While these so-called ‘sin taxes’ primarily target consumption behaviour, they also affect household budgets directly.

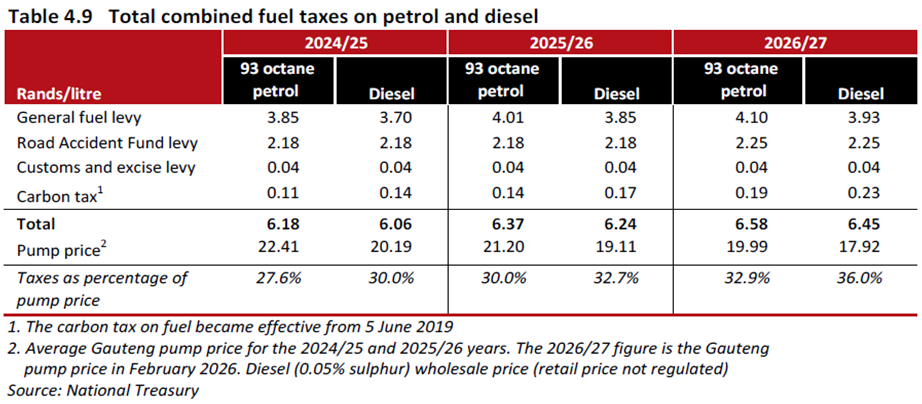

Fuel levies and the carbon fuel levy adjustments add incremental pressure on petrol and diesel prices. Since fuel costs feed into transport, food distribution, and logistics, indirect price increases are likely to affect most consumers.

Lower-income households tend to feel these increases more sharply because essentials consume a larger share of their income.

WRITTEN BY STEVEN JONES

Steven Jones is a retired tax practitioner and member of the South African Institute of Professional Accountants.

While every reasonable effort is taken to ensure the accuracy and soundness of the contents of this publication, neither writers of articles nor the publisher will bear any responsibility for the consequences of any actions based on information or recommendations contained herein. Our material is for informational purposes.